A Self‑Invested Personal Pension (SIPP) is a type of pension designed as a tax-efficient way to save for retirement. A SIPP is a type of personal pension that you open and manage yourself. You choose how much to contribute, when to contribute, and how your money is invested. Eligible contributions receive basic rate tax relief once HMRC has processed them, helping your pension grow over time. The amount of tax relief you receive depends on your individual circumstances and the rules in place at the time.

The Quilter Invest SIPP is designed to help you build your pension savings over time. When you reach retirement age, you’ll be able to access your pension in line with the options available at that time, which may include drawdown or transferring to another provider.

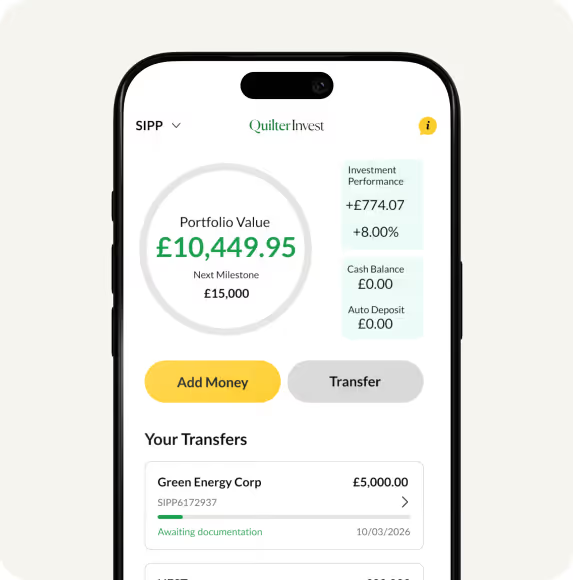

With the Quilter Invest SIPP:

- Basic rate tax relief is applied at 20%. This means that for every £80 you contribute, £100 is added to your SIPP, a 25% top up to your contribution. Quilter Invest claims this tax relief from HMRC on your behalf and adds it to your pension automatically, usually within 6 to 8 weeks.

- You can transfer existing pensions into one place to help you manage your retirement savings more easily.

- You can invest in Quilter’s professionally managed MyGoal funds, designed to suit a range of risk levels and investment goals. View MyGoal funds.

- If you set up Auto Invest, any tax relief you receive can be reinvested automatically in line with your chosen investment strategy.

The amount your pension is worth depends on:

- The performance of your chosen investments

Quilter Invest does not offer financial advice. We cannot advise you on whether a SIPP is right for you, how much you should contribute, or which investments are suitable for your circumstances. The value of investments can go down as well as up, and you may get back less than you have paid in.

If you are unsure whether a SIPP is right for you, you should speak to a financial adviser. You can book a free consultation here: Book a consultation | Quilter. This consultation is provided by a financial adviser and is separate from Quilter Invest.